- Australia and Singapore are the most exposed to China growth due to strong economic linkages via the commodity and trade channels, respectively.

- The Philippines and India are the least exposed due to weak trade and investment linkages with China.

- The spillover from China to the rest of Asia has weakened over the last decade due to the fall in Asia’s export share to China.

- China’s policy blitz

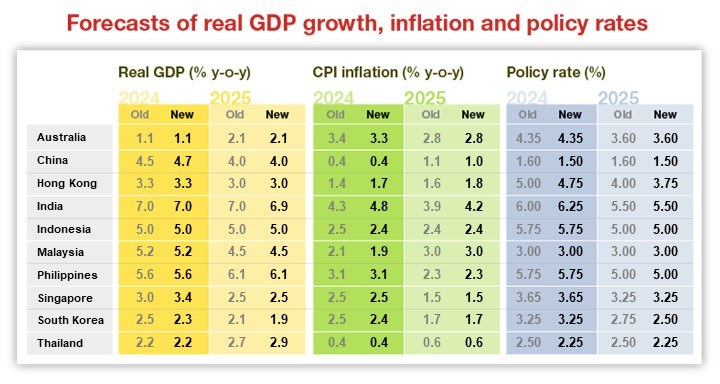

- China’s recent stimulus blitz is the latest addition to the various uncertainties weighing on Asia’s economic outlook. Since September 24, the nation has announced monetary policy easing, liquidity support for equity markets, government pledges to arrest the property market decline, and reports of fiscal support in the pipeline. Nomura’s China economics team has lifted its Q4 2024 GDP forecast to 4.4% year-over-year while retaining its 2025 GDP growth forecast at 4%. As the contours of China’s policy support and its economic impact are still laced with uncertainty, we revisit Asia’s China exposure.

- Similar, but different

- To assess the overall impact of China’s economy on the rest of Asia, we combine four major economic channels of goods and services exports, terms-of-trade effects from commodities, foreign direct investments, and financial markets into a single scorecard.

- Exposure to China: Our analysis show that Australia and Singapore are the most exposed to China growth due to strong economic linkages via the commodity and trade channels, respectively. On the other hand, the Philippines and India are the least exposed due to weak trade and investment linkages with China.

- Coupling versus decoupling: The spillover from China to the rest of Asia has weakened over the last decade due to the fall in Asia’s export share to China. Our analysis shows that Australia and Thailand have become even more coupled to China cycles, while South Korea has decoupled somewhat.

- China stimulus type: Asia’s exports to China are most sensitive to the country’s property construction investment, followed by its retail consumption. Meanwhile, Asia’s exports are least sensitive to China’s infrastructure investment. If Beijing announces faster construction of infrastructure projects such as railways and power grids, Asia may benefit less. However, if property investments increase as a result of fiscal stimulus for the property sector, it could broaden Asia’s exports recovery and lift commodity prices.

- China exporting inflation or deflation: Typically, any China stimulus is seen as inflationary for Asia. If China stimulus is aimed more at the supply side, such as more incentives or loan support for manufacturing, this can exacerbate existing overcapacity issues over time. Asian imports from China have already jumped significantly, spanning low-end consumer goods to high-end electric vehicles. Western tariffs on Chinese exports are likely to redirect these exports to Asia. Thus, while a real turnaround in the property sector can be inflationary, there is a lower bar to China exporting deflation to the rest of Asia.

- China’s market spillovers: In the short term, Nomura’s equity strategists note that there is a possibility of further rotations as investors fund their reallocations to China to more neutral weightings by paring India, Southeast Asia, and even Korea. For currency spillovers, Hong Kong has the highest correlation with China’s equity index due to its status as the financial gateway to China. In addition, the CNY/USD correlation is high and so it is for the following Asian currencies versus USD: Singapore dollar, Thai baht, and Australian dollar.

- Country-specific comments

- Southeast Asia

- Singapore remains among the most exposed to China’s economy, particularly via the export and foreign direct investment channels, followed by Malaysia, which has the additional exposure as a commodity producer. Indonesia’s exposure has increased over the last few years, thanks to processed nickel exports, but it is still comparatively low within the region. China’s industrial overcapacity suggests this will remain a drag on Indonesia’s overall commodity exports. Thailand’s exposure ranks in the middle of the pack and comes from its reliance on tourism and the relatively high share of visitors from China. The Philippines has the lowest exposure, more so in recent years, in part because of limited FDI inflows from China and supply chain re-orientation benefits.

- Australia

- China remains Australia’s largest trading partner by a wide margin. Any improvement in China’s growth should result in stronger real GDP growth for Australia, particularly via higher export volumes. Most significant impacts would likely be felt on the nominal side rather than the real side via higher bulk commodity prices, higher company tax and royalty collections, and stronger budget and trade balances. Australia runs a healthy trade surplus with China. Amid other global uncertainties, a better China scenario might not unleash a round of major mining capital expenditure expansion plans as businesses are likely to remain cautious for some time. It is worth noting that mining accounts for only 2% of total employment in Australia.

- India

- India ranks low on economic and financial market linkages with China, although India equity markets have fallen amid foreign investors reprioritizing in favor of China’s markets. China is not a key market for Indian exports, as India runs a sizeable merchandise trade deficit with China. This potentially opens up two channels of impact. First, India has been routinely levying anti-dumping duties against Chinese imports. If China’s property sector revives, it may help alleviate the issues around dumping as the sector starts to absorb the excess capacity. Secondly, a potential revival of China’s property sector and its broader economy could drive a strong demand increase across global commodity markets and lead to higher input costs for Indian companies. Higher commodity prices globally could drive an incremental pick-up in core goods inflation, delaying India’s monetary policy easing.

- South Korea

- Korea’s exposure to China has decreased as its trade surplus with China shifted to a deficit in 2023. While China remains among the top two trading partners, its share of Korea’s total exports has continued to decline. Korea’s auto and electric vehicle battery industry have become a large importer of raw materials from China, while China has steadily cut back on imports from Korea in favor of domestic industries. Korea’s central bank estimates that the sensitivity of Korea to China GDP growth has declined significantly. On inflation, positive fiscal and credit stimulus from China can increase the upside risks in Korea through the supply-side channel, such as via higher raw material prices.

{kind=link}