Donald Trump has won the US presidential election. Tariffs and tax policy will likely be the focus under Trump 2.0, according to Nomura analysis. The administration may implement 60% tariffs against China, which may come into effect by mid-2025, and baseline tariffs of 10% on most foreign products imported by the US.

What Trump 2.0 means for Asia

Asia is better prepared this time. Trump’s re-election has less of a shock factor given greater familiarity with his policies. Asia is also more resilient, due to the ongoing trends of US-China decoupling, shifts in global supply chains and lower Asian exports to China. Yet, Trump 2.0 will likely mean more policy uncertainty, which may be a negative for Asia.

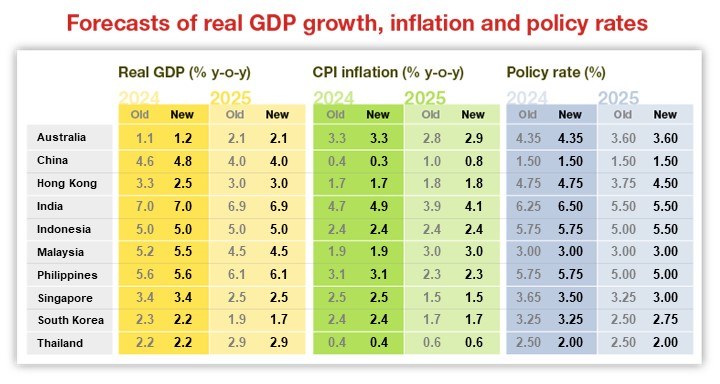

There could be a larger drag on 2025 GDP growth. Even prior to the US elections, Nomura’s leading indicators on exports and memory prices suggested an impending slowdown in Asia’s export growth, as well as growing evidence of softening domestic demand in India, Thailand and South Korea. Though some front-loading of exports is possible ahead of the actual tariff implementation, weaker global growth could slow Asian exports in the second half of 2025.

There could also be more disinflation ahead for Asia due to weaker growth, more economic slack, lower energy prices and the risk of more Chinese exports flooding Asia. Inflation could be lower by 0.1-0.2 percentage points in 2025, relative to Nomura’s current baseline estimates.

Some economies may be supply chain beneficiaries. A 60% tariff on Chinese exports to the US can lead to import substitution, with Southeast Asian economies having a potential advantage. It could also lead to trade diversion in which China routes exports through other countries, although there is a risk that this could prompt greater scrutiny under Trump 2.0. Supply chain diversification will continue in the medium term, with India and Malaysia likely to be the big beneficiaries in the electronics and semiconductor sectors.

Trump’s protectionist stance will further the US-versus-China-centric regional blocs. Under Trump 2.0, we expect China-ASEAN trade and investment integration to strengthen, while India, Australia, Japan and South Korea appear more closely aligned to the US.

Policy implications

Nomura’s US economists expect that tariffs will generally be a negative for the US economy, leading to lower growth and adding roughly 0.75 percentage points to US inflation in 2025. As the Fed is likely to pause its rate cutting cycle during a tariff-driven inflation spike, Nomura’s US economists now expect only one cut in 2025 after cutting once in December 2024, leaving the fed funds rate at 4.125% at the end of 2025.

The policy response in Asia may be more nuanced.

Trump’s victory increases the downside risk to China’s export growth and will likely lead to a larger stimulus package from Beijing. With fewer Fed rate cuts, an increased likelihood of Japanese yen depreciation and recent hawkish rhetoric from Bank of Japan Governor Kazuo Ueda, we expect a 25-basis-points hike in December by the Bank of Japan, followed by 25-basis-points hikes in each of April and July next year.

Asia will also see more monetary policy divergence. Slower growth and disinflation call for more policy easing, but higher US terminal rates and tighter global financial conditions would create a tricky environment for Asian central banks that are more sensitive to Fed and FX-related risks, such as Bank Indonesia and Bank of Korea. For other Asian central banks, we expect policy decoupling from the Fed.

Winners and losers

While the broader economic and geopolitical impact of Trump’s victory is negative for Asia, especially for China and South Korea, Nomura’s economic analysis shows that India and Malaysia should be relative beneficiaries.

China is directly in the line of Trump’s fire. South Korea is likely to be adversely impacted due to weaker growth and headwinds for the Korean electric vehicle and battery industries. On the other hand, India and the US share deep economic and strategic interests, which may bode well for the Asian country. Similarly, Malaysia may benefit over time from higher foreign direct investment inflows from multinational corporations looking to diversify their supply chains.

{kind=link}