The growth of the Chinese economy over the last four decades is one of the most globally transformative events of the last few centuries. Beginning in 1979, the country has radically transformed from an agrarian economy to one dominated by service and industry, and China stands today as the world’s top trading nation. Recently, however, this “growth miracle” has shown signs of weakening. Even before the country’s COVID shutdowns, growth had begun stalling amid demographic headwinds, an emerging slowdown in the real estate sector, and a re-emergence of state-led economic policymaking. The centralization of power has fed into a worsening relationship with China’s western partners that further threatens the country’s growth prospects.

China’s government began to play a larger role in private enterprise in the 2010s, feeding into a worsening relationship with the West.

The Facts:

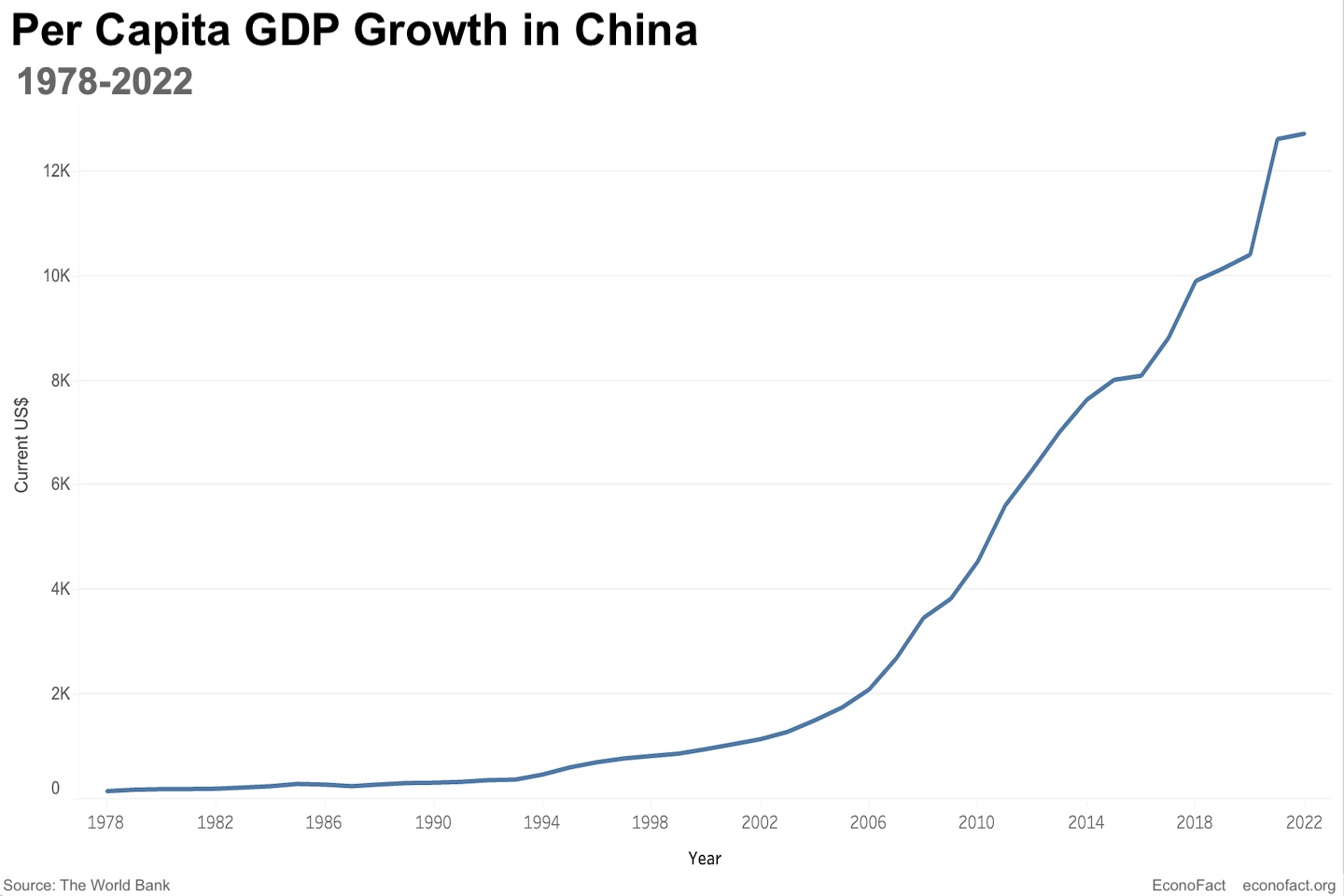

- In a little over four decades, China went from being one of the poorest countries in the world — with a real per capita GDP of only $156 US dollars in 1978 — to joining the ranks of upper-middle-income countries with a real per capita GDP of $12,720 in 2022 (see chart below). The growth is particularly striking considering the country’s population size, sweeping territory, and vast heterogeneity. According to national income criteria established by the World Bank, China became a lower-middle-income country in 2001 and transformed into an upper-middle-income country in 2010. Comparing China’s real per capita GDP to the US’s in purchasing power parity (PPP) terms, which takes into account differences in the two countries’ costs of living, China’s has grown from 4.1% of the US per capita GDP level in 1990 to 28.4% of the US level in 2022.

- The Chinese economic growth miracle was, to a large extent, a result of the country’s embrace of market-oriented reforms and globalization. The establishment of formal diplomatic relations with the United States in 1978 paved the way for a virtuous cycle whereby China’s internal reforms gradually decentralized economic decision-making, introduced the market as an increasingly important mechanism for resource allocation, opened the door to foreign investment and significantly increased international trade, which in turn helped to foment further market-oriented changes. The first major reform was the introduction of the household responsibility system, which gave farmers greater autonomy in decision-making. In the 1980s, special economic zones were established in coastal areas. Together with new “open-door” policies, these zones attracted foreign investment and experimented with market-oriented policies. In addition, price reforms were gradually implemented, starting in 1979. In 1992, in its 14th National Congress, the Chinese Communist Party formally incorporated the idea of a market economy into China’s socialist ideology. New reforms — including changes to state ownership of enterprise, the legal system, fiscal policy, and the central bank, as well as the establishment of factor markets, a social safety net, and a personal income tax —made a hybrid market system the economy’s main operating system rather than a mere supplement to central planning. These sweeping and historic market-oriented reforms led to China’s 2001 accession to the World Trade Organization (WTO), which further committed China to additional market liberalization and integration into the global economy. China’s global trade soared and, by 2007, China’s exports had risen to 32 percent of GDP.

- Large productivity gains powered China’s economic growth until 2007. Between 1990 and 2007, China’s productivity grew at an average rate of 4.5% per year. The periods with the fastest productivity growth coincide with the rapid growth of town and village enterprises in the mid-1980s, the state-owned enterprise reform in the mid-1990s, and the explosion of Chinese foreign trade and inbound foreign investment following China’s WTO entry in 2001. Large scale reallocations of labor from agriculture to the manufacturing and service sectors, and of capital from the less-productive state-owned enterprises to more productive private firms, contributed to the growth in productivity.

- Since 2007, China’s productivity growth has stalled at just about 1 percent per year. The global financial crisis of 2007-2009, which originated from the large-scale default of subprime mortgages in the US housing market, shook China’s confidence in the Western-style financial system and may have served as a catalyst for the resurgence of the state-owned enterprises. Before 2008, Chinese local governments were not allowed to borrow; but a 4 trillion RMB stimulus allowed local governments to borrow via local government financing vehicles and become drivers of investment, crowding out private-sector investment (see here). The Four Trillion RMB stimulus rolled out in 2008, followed by an infrastructure investment and housing boom, sustained China’s economic growth rate at around 10 per annum until 2011. But these debt-financed investments also planted the seeds for the debt problems Chinese developers and local governments are currently facing.

- Beginning in the 2010’s, the Chinese government began to play a larger role in private enterprise in three aspects. First, the government began controlling small stakes in many private firms. While the share of 100% state–owned firms has been declining over time, the share of firms with at least a 10% stake from the state has risen from roughly 50% to 60% from 2012-2017. Second, Chinese party leaders have taken a larger role in corporate governance. In 2002, less than 27 percent of private companies contained a party cell. But by 2018, China’s regulators made the establishment of Party cells a requirement for any company to be listed on domestic stock exchanges. China’s top leaders have become increasingly explicit about their expectations for increased Party engagement in private companies, calling for Chinese Communist Party cells to better understand and interact with private companies and to help “improve their corporate governance structure”. Finally, beginning in 2020 Chinese leaders began to take a much tougher regulatory line with Chinese domestic businesses than had previously been evident. In November 2020, for example, the IPO of Ant Financial was abruptly suspended following a speech by Alibaba chairman Jack Ma that criticized China’s financial regulators for being too conservative. While there were regulatory rationales for most crackdown’s these rules were not rolled out with China’s usual deliberation and were seen as arbitrary by many in selectively targeting certain sectors and firms, primarily private firms rather than state-owned enterprises.

- Research suggests that China’s increasingly prescriptive industrial policy may have had limited success in promoting productivity. Several studies find instances in which government subsidies did not result in productivity-enhancing breakthroughs. For example, rather than encourage innovation, tax incentives to firms that surpassed certain R&D investment thresholds resulted in administrative expenditures being relabeled as R&D. Another study found little evidence that the Chinese government had consistently picked winners when allocating subsidies; and, researchers of Japanese economic history have found that while industrial policy may be effective when a country is trying to catch up, it is unlikely to be effective when a country aims to lead the frontier (see here). Moreover, the state-equity presence, rising presence of state cells in corporate governance, and increase of regulatory crackdowns make state intervention more likely in unusual circumstances, as when, for example, regime stability or national security is at stake. The Chinese government’s recent tendency to rapidly engineer policy U-turns hurts confidence. This possibility makes it more difficult for Chinese businesses to attract foreign investment and has become a key barrier to the international-market expansion of Chinese firms like TikTok and Huawei.

- Amid a worsening relationship with the US-led West, the Chinese leadership has further turned to more centralized decision-making and slowed down the implementation of the market-oriented reform agenda that was passed in the third plenum of the 18th CCP congress. From 1979 to 2008, the US and China were engaged and friendly. Occasional flare-ups were dealt with diplomatically and did little damage to the long-term warm bilateral relationship. Today, however, the US-China relationship is at its lowest point in the last 40 years. The change became evident in President Obama’s “Pivot to Asia” in 2011 and intensified with President Trump’s anti-China campaign-rhetoric and the trade war initiated in 2018. The economic relationship between the two countries is now intertwined with national security concerns. The US has instituted restrictions on both outbound investment in Chinese firms and inbound capital flows from China to protect against intellectual property theft from China. The total bilateral Foreign Direct Investment between the US and China fell to $15.9 billion in 2020 amid pandemic-related disruptions and rising tensions in the US-China relationship. These restrictions, along with US embargoes of key technological goods like semiconductors and smartphone processors, have further hampered growth of Chinese firms – most notably, Huawei.

What this Means:

The Chinese growth miracle was driven by market-oriented reforms and an opening of the country’s previously-closed economy to the world. China faces important structural issues today, such as slowing productivity growth and an aging population that threaten future growth prospects — beyond the recovery from pandemic-induced shocks and a severe contraction in its construction sector. However, these structural issues could be tackled more effectively by market-deepening reforms and, if this were to be the case, I believe that China could continue to have a growth potential of up to 6% per year for the next 10 to 15 years. However, whether China can realize such growth potential will likely depend largely on how leaders manage its internal political economy — specifically whether the state continues to play a large role in economic decision-making — and the relationship between China and the US-led West, which will determine China’s access to foreign technology, finances, and markets. If leaders continue the turn away from market-oriented reform in favor of centralized decision-making, top-down planned resource allocation, and marginalizing private businesses, then productivity and economic growth could deteriorate further. China, the United States, and the world would all suffer as a result.